Japan builds its CFIUS: Broader scope, deeper scrutiny

Japan is tightening foreign investment review, but the larger shift is institutional. A regime once focused on formal filings is becoming more substantive, intelligence-led and security-driven.

In brief

Japan’s foreign investment regime is moving into a more assertive phase. A bill to amend the Foreign Exchange and Foreign Trade Act (FEFTA), now approved by Japan’s parliament, will bring certain indirect acquisitions into scope, expand post-closing intervention powers and formalize a broader inter-ministerial review framework sometimes described as a “Japan CFIUS.”, combining to create a materially more substantive environment for investors in sensitive sectors. At the same time, Japan is expected to reduce the filing requirement for lower-risk areas, freeing up resources to focus on more problematic investments.

Japan’s foreign investment regime is being recalibrated for a less benign world. The country remains open to foreign capital, and the government continues to stress the importance of sound investment. But openness now comes with a sharper security filter focused on specific countries and certain asset types.

That shift predates Prime Minister Sanae Takaichi’s appointment in October 2025. Japan has been moving steadily toward a more economic security-focused model for several years, with greater scrutiny of sensitive technologies, critical infrastructure, data and supply chains. The latest reforms accelerate that trend. They also make the review process less about the formal route by which the investment is made and more about the substance of influence, control and access to security information.

The resulting regulatory environment is something more nuanced and more challenging for investors, who cannot so easily test issues most relevant to the government’s assessment such as foreign government influence.

A wider lens on control

The amendment to FEFTA is expected to make three practical changes that matter most for investors.

First, certain indirect acquisitions will become reportable. At present, Japan’s FDI regime focuses largely on direct acquisitions of shares or voting rights in Japanese companies. That leaves a gap where control over a Japanese business is acquired indirectly through a foreign holding structure. The amendment is designed to close that gap.

Two types of indirect acquisition are expected to become reportable. The first is the acquisition, directly or indirectly, of 50% or more of the voting rights in a foreign entity that itself holds certain interests in a Japanese company. The second is the exercise of voting rights to appoint board members in that direct holder or its parent, where the result is that the foreign investor and related persons gain majority board control.

Investors acquiring non-Japanese companies will need to look through the structure and identify whether the target group holds interests in Japan. Board appointments in foreign entities may also require FDI analysis if those entities sit above Japanese assets.

This is a material change for cross-border M&A. Japan may no longer be a secondary diligence point simply because the immediate target is outside Japan.

Call-in risk

Second, regulators are expected to gain broader call-in powers including post-closing.

Under the current regime, Japanese authorities have limited formal ability to review investments outside the listed sensitive sectors that require prior notification. In practice, regulators have not always been passive. They have used informal channels to raise concerns and influence outcomes. But the amendment will give a clearer legal basis for intervention where a transaction that did not require prior approval can be considered to raise national security concerns.

The new call-in power is expected to apply for up to five years after closing. It would be limited to certain categories of investment, including direct acquisitions of listed and unlisted companies, mergers and business transfers. Indirect acquisitions appear to be outside the scope of this particular post-closing power on the face of the legal text, but actions may be taken in a more informal manner for indirect acquisitions too.

For investors, the message is not that every non-sensitive Japanese investment becomes risky. It is that “not notifiable” will not always mean 'beyond scrutiny'. Where a transaction touches sensitive technology, data, infrastructure or strategic industrial capability, investors may need to consider early informal engagement even if no mandatory filing is triggered.

The exact modality for informal engagement has not been established yet, including how much clarity investors can obtain and when. This is to be further developed after the reforms are in place.

Lower-risk filings may be narrowed

Third, Japan appears to be trying to reduce unnecessary burden in lower-risk areas.

The current regime captures a wide range of transactions, including some that present little obvious national security risk. That has contributed to a heavy volume of prior notifications and has made the regime less targeted than policymakers may now want. Discussions are underway to rationalize the designated sectors requiring prior notification, particularly in areas such as information technology where current definitions can be broad.

The bill itself does not appear to set out the detail of this rationalization. Such changes are more likely to come through subordinate regulations, notices or guidance.

This is the other side of the reform. Japan is not simply expanding review. It is trying to distinguish more clearly between routine investment and transactions that warrant close examination. If implemented well, this should reduce friction for benign investments. On the flip side, it also potentially means that transactions that do attract scrutiny may face a more intensive review.

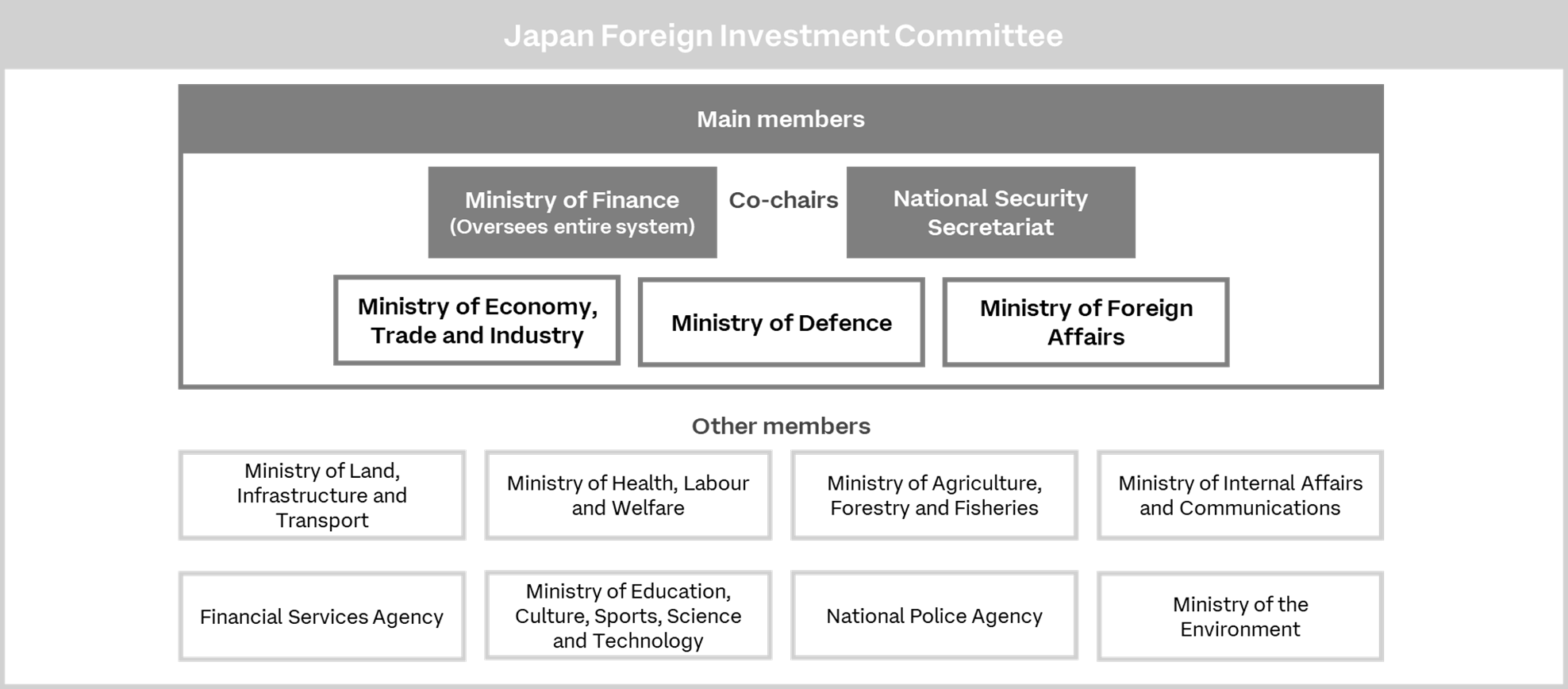

”Japan CFIUS”

The institutional reform may matter as much as the legal thresholds.

The government is moving toward more institutionalized intelligence gathering and sharing, following the model used by the CFIUS regime in the US.

The Minister of Finance and the ministers responsible for relevant business sectors will be able, where necessary, to seek opinions from the Prime Minister, the Minister for Foreign Affairs and other relevant authorities. In practical terms, this will mean a wider group of security, diplomatic and sectoral agencies can feed into the FDI review.

This will likely change the character of the process. Reviews may become less formalistic and more intelligence-led. Regulators will be better placed to assess indirect foreign government influence, potential technology leakage, data exposure, supply chain vulnerability and risks to critical infrastructure.

For transaction parties, this creates a familiar problem in a new setting. The issues that matter most to the government may not be visible to the transaction parties. Review timetables may be affected by information the parties do not have and cannot easily test. Sensitive transactions may therefore feel less predictable, even where the legal rules are clearer.

Overview of Japan CFIUS

Source: Liberal Democratic Party website.

Enforcement is moving first

Japanese regulators have been issuing more detailed requests for information, including questions designed to probe links with particular governments or state-linked interests. More transactions also appear to be subject to ring-fencing or other mitigation measures as a condition of clearance.

Public statistics have not fully reflected the rapid uptick of enforcement. This is because Japanese authorities often use administrative guidance - such as informal, nonbinding requests - that encourage parties to modify, delay or abandon transactions before the process escalates to a formal prohibition or remedy order. That tool gives regulators flexibility and insulates diplomatic sensitivity. Some transactions may be stopped or reshaped without appearing in official prohibition statistics.

The proposed acquisition of Makino by MBK Partners shows how far the regime can go when sensitive technology is involved. In April 2026, the Japanese government opposed MBK’s bid for Makino, a leading machine tool manufacturer with technology used in defense-related applications. This is the first time in 18 years that the government used its official powers to block a foreign investment. The government stressed that restrictions on foreign investment should be minimal as a rule. In the case of MBK Partners, however, Makino’s dual-use machine tools were deemed too sensitive to be acquired by a foreign entity.

Japan has not suggested that foreign investment is unwelcome. It has drawn a harder line around assets it sees as strategically sensitive. For investors, that line will not always be obvious at the outset.

Security logic is spreading

The same security logic is beginning to influence adjacent areas of policy. The Japan Fair Trade Commission has published guidance and case materials addressing national security considerations in merger review. Those materials suggest greater willingness to recognize industrial resilience and technology protection as relevant policy concerns.

Corporate takeover policy may also move in the same direction. The Ministry of Economy, Trade and Industry is considering whether national security concerns should be reflected in target management’s assessment of competing bidders. If that approach develops, national security may become part of a target board’s judgment about a prospective deal as well as regulatory review.

This is the broader point. Japan’s FDI reforms are part of a wider reordering of economic policy around national resilience. Competition law, takeover policy and investment screening are not merging into one regime. But they are increasingly being pulled by the same gravitational force.

June 2026 articles

Past editions & articles

Looking ahead

Japan is not closing itself to foreign investment. It is asking a harder question: when does investment become strategic influence which needs to be addressed?

For investors, four practical points follow:

- Screen for Japanese interests across the full group structure, not just the immediate target.

- Treat indirect control, board appointment rights and foreign government links as early diligence issues.

- Build potential FDI engagement into deal timetables where sensitive technology, data or infrastructure is involved.

- Do not assume that a non-notifiable transaction is insulated from later review.

The landscape is clearly shifting. Low-risk investment may become easier to process. Sensitive investment will likely entail detailed scrutiny and require a coherent narrative as to why it does not raise national security concerns.

With thanks to Freshfields Kaori Yamada, Yusuke Kanbayashi and Shuntaro Muto for their contributions to this update.